2025 Showed the Gap Between Early Promise and Real Adoption

Throughout 2025 it’s grown increasingly clear which projects are truly appealing to the needs and requirements for onboarding institutional capital. From operating real payment and settlement rails across live corridors, we saw directly where early narratives held up under volume and where they broke down once systems were put into production.

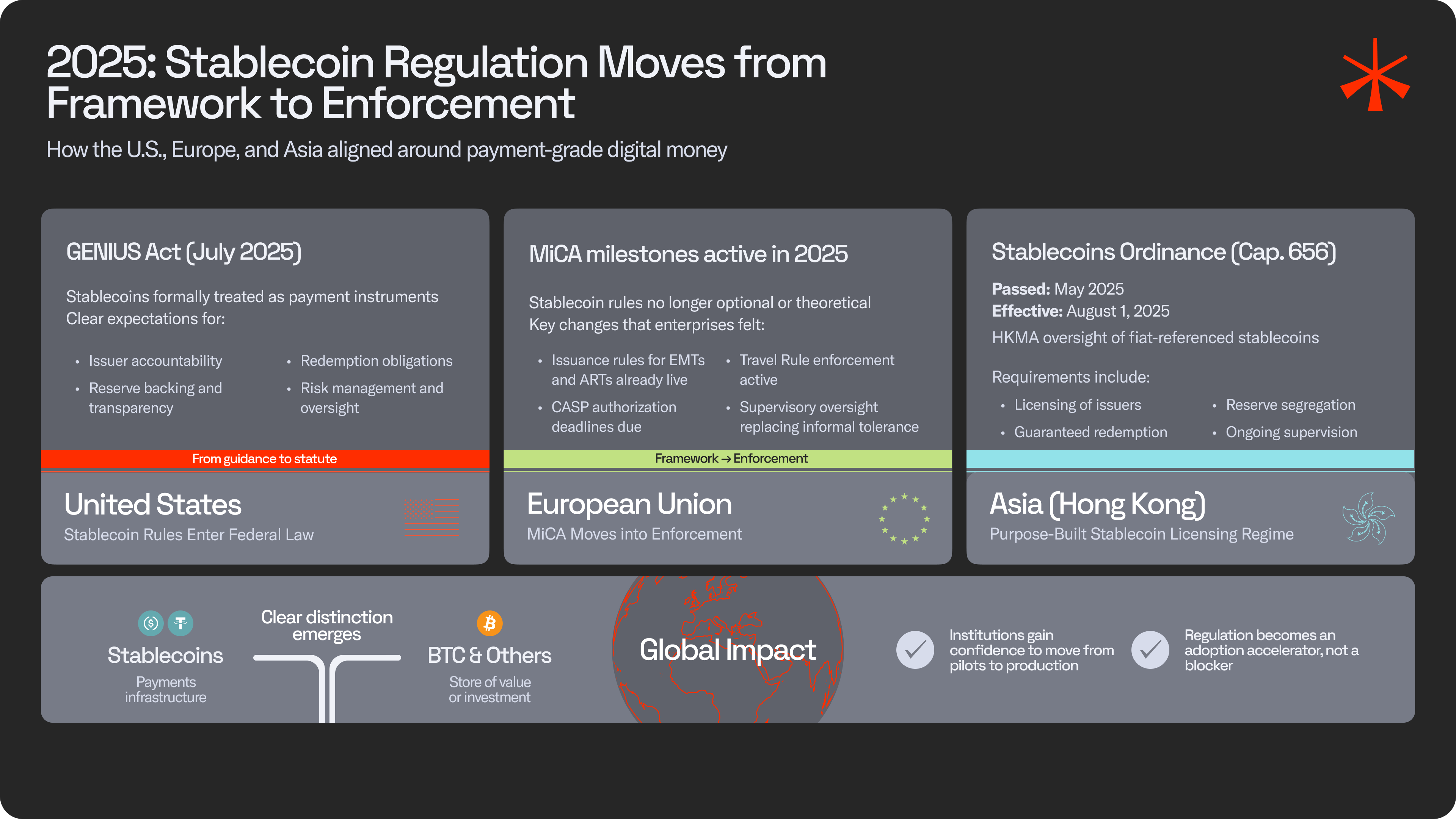

The GENIUS Act was signed into law in July and the CLARITY Act also passed the House in July. Stablecoins are a primary pillar of crypto’s product-market fit, serving as monetary equivalent assets that move outside the limits of borders and calendars.

We expect 2026 to be marked by crypto continuing to mature. Where 2023 and 2024 were largely defined by pilots, proofs of concept, and limited-scope experimentation, 2025 marked a shift toward production systems expected to process live payments consistently, at scale, and under regulatory scrutiny.

Enterprise teams have begun seeking products that process real payments, demonstrate resilience, and earn the trust they seek. Reliability, reach, and ability to integrate with modern payment rails have been key indicators of success for this year.

The GENIUS Act, in particular, matters because it cements operational requirements, issuer accountability, and reserve transparency requirements. Among regulatory hurdles collapsing, staking ETFs are on the horizon for BlackRock and other firms, while Grayscale received its first staking ETF approval in October.

Stablecoin and RWA Infrastructure Finally Became the Story, Not the Slogan

2025 was the year when stablecoin and RWA platforms were no longer evaluated on the elegance of their pitch decks, but on the stability and behavior of their underlying rails. As regulatory clarity solidified, institutions stopped entertaining theoretical models and focused on systems that could move value predictably across borders, systems, and counterparties.

Stablecoins emerged as the cleanest monetary primitive for this environment. They’re programmable and settlement-ready, in addition to being able to handle the operational demands that traditional payment stacks struggle to meet.

Funding and engagement for aspirational projects have decreased substantially. A growing number of teams learned that distribution, uptime, and settlement behavior were the real value drivers. The platforms that gained ground were the ones that shipped dependable, interoperable rails and demonstrated that tokenized liquidity could move cleanly across markets.

Regulatory Clarity Created Winners and Forced Hard Conversations

Regulatory developments throughout 2025 didn’t just reshape compliance expectations; they reshaped competitive dynamics.

In Europe, MiCA stopped being something for teams to “plan around” and became something they had to operate within. Stablecoin issuance rules tied to e-money and asset-referenced tokens were already live, while CASP authorization deadlines, travel-rule enforcement, and supervisory expectations were due across 2025.

The GENIUS Act defined some baselines for issuer behavior, reserve construction, risk management, and transparency. With that baseline established, it has become easier for institutions to identify which issuers were prepared to operate under scrutiny and which were not.

In Asia, Hong Kong moved decisively toward a purpose-built stablecoin regime. In May 2025, the Legislative Council passed the Stablecoins Ordinance (Cap. 656), establishing a licensing framework for fiat-referenced stablecoin issuers under the supervision of the Hong Kong Monetary Authority.

The regime formally came into effect on August 1, 2025, with requirements covering issuer authorization, reserve segregation, redemption guarantees, and ongoing supervision.

Global clarity benefited well-structured platforms and applied pressure to everyone else. Even developments adjacent to crypto’s core, like the progress of staking ETFs, reinforced that regulators' shifts toward more structured oversight and higher operational standards. For many teams, 2025 was the year when sidestepping regulation ceased to be a viable strategy.

Institutions Moved Quietly, But Their Criteria Got Sharper

Institutional interest in 2025 was steady, deliberate, and noticeably more sophisticated.

Instead of experimenting broadly, enterprise teams concentrated on providers that can pass deeper operational due diligence. They evaluated settlement behavior under load, cross-border route reliability, reserve disclosure quality, and the ability of platforms to integrate without disrupting existing treasury or payment workflows.

Security and resilience transitioned from being differentiators to minimum requirements.

Platforms that met those thresholds earned meaningful pilots and long-term commitments. Those who could not were filtered out early, often without a second conversation. By the end of the year, the market had a clearer sense of what “institutional readiness” actually meant, and the path to adoption had narrowed accordingly.

2025 has increasingly solidified the role of bitcoin as a store of value, particularly as stablecoins have transitioned to become more of a pure fit for fintech operations. The distinction of “payment stablecoins” seems to have been one of the biggest delineations of this year.

2025 Was the Year Distribution Outpaced Innovation

2025 marked a turning point in how platforms earned institutional attention. The most successful teams weren’t the ones announcing new primitives; they focused on expanding distribution, strengthening connectivity across chains and geographies, and proving that programmable money can operate reliably on top of the rails enterprises already trust.

Stablecoins continued to link fragmented markets into a more unified liquidity landscape. By 2025, hundreds of billions of dollars in stablecoin volume were settling monthly, much of it tied to payments, treasury movements, and working capital cashflows rather than speculative trading.

This was the year distribution became the core competitive advantage.

Existing Rails Proved Sticky, but Multichain Distribution Became Mandatory

SWIFT, SEPA, and domestic clearing networks (e.g., UPI, M-Pesa) remained deeply entrenched across enterprise workflows. Combined, these channels cleared trillions of dollars in transactions across 2025. Treasury teams didn’t abandon them; they layered programmable liquidity on top of them. What changed in 2025 was the expectation that platforms had to operate across both traditional and on-chain environments without friction.

Multichain distribution across EVMs, L2s, and emerging high-throughput networks like Solana shifted from a competitive edge to a default requirement. Enterprises wanted access to new liquidity paths, but not at the cost of reliability. Providers who could bridge those constraints earned the right to scale.

API-First Platforms Won Market Share

A significant share of adoption in 2025 shifted to API-first platforms that addressed the operational problems enterprises actually face, including onboarding complexity, compliance workflows, treasury integration, reconciliation, cross-border settlement, and FX complexity. These teams outperformed by dissolving friction.

Enterprises gravitated toward partners that made programmable money accessible without requiring them to rethink their entire infrastructure stack. This has been a year defined by institutional practicality and usability.

Tokenized T-Bills Matured into a Global Liquidity Primitive

2025 was the first year tokenized T-Bills behaved like a genuine global liquidity primitive rather than an experiment. Real volume arrived. Institutional flows diversified across issuers. On-chain Treasury funds crossed into the tens of billions in assets. Risk teams became more comfortable with the underlying mechanics, and treasury desks began incorporating on-chain money markets into their short-term allocation strategies.

Product-level maturity supported a broader shift toward programmable liquidity: stablecoins for payments, tokenized T-Bills for yield and capital efficiency, and unified settlement layers that could manage both. Initially a niche innovation in prior years, these evolutions of global liquidity are becoming foundational building blocks for global cash management.

2025 Consolidated the Ecosystem into Fewer, Bigger Trust Anchors

By the end of 2025, the market had begun to coalesce around a smaller number of highly credible platforms, those that demonstrated operational maturity, transparent governance, and the ability to integrate cleanly into global payment and treasury workflows. Institutions moved away from fragmented vendor stacks and toward partners that had proven reliability across jurisdictions and rails.

This consolidation echoed a broader pattern already taking shape across global payments, where trust anchors, rather than theoretical innovation, defined scalability.

Market Flight to Quality Redefined “Blue Chip” in Digital Assets

2025 reshaped what “blue chip” meant in digital assets. Branding, ecosystem size, or early-mover stories no longer carry the same weight. Instead, institutions concentrated on issuers and platforms that could consistently meet higher operational and regulatory standards; transparent reserves, predictable redemption behavior, audited governance structures, and strong treasury controls.

The projects that rose into the new “blue chip” category did so because they reduced uncertainty, not because they generated attention. As institutional due diligence sharpened, credibility became a function of demonstrated discipline, not narrative strength.

Vendor Overload Pushed Enterprises Toward Unified Platforms

Many enterprise teams entered 2025 with sprawling vendor stacks and multiple integrations for compliance, wallets, payments orchestration, reconciliation, reporting, and treasury operations. That fragmentation resulted in expanding liability, as systems were strained with cross-border scale and emerging regulatory requirements.

In response, companies began consolidating around unified platforms, like Noah, that reduced brittle touchpoints and provided clearer ownership of the payment surface. Enterprises prioritized resiliency, governed integrations more strictly, and favored providers who could collapse multiple workflows into cleaner, more dependable rails.

The outcome was a structural shift: fewer partners, deeper integrations, and more disciplined vendor governance.

Cross-Border Payments Became the Largest Real-World Proof Point

While Western markets focused primarily on market structure debates, the most meaningful adoption emerged across Africa, LATAM, and MENA. Businesses in these regions used stablecoins and tokenized liquidity to bypass delays, FX friction, and settlement limitations that had constrained them for decades.

These markets demonstrated what programmable money could do when it addressed urgent, not hypothetical, problems. Faster settlement, predictable routes, and reduced operational overhead provided tangible proof that digital dollars and unified liquidity rails could outperform legacy corridors in everyday commerce.

For the first time, cross-border payments were the strongest real-world validation of programmable financial infrastructure.

2026: Rails Will Get Real

Payments Transition Into Production Environments

2025 was defined by clarity about infrastructure readiness, distribution strength, and the consolidation of trust. 2026 is poised to be defined by execution. The foundations are in place. Enterprise expectations have sharpened. Cross-border corridors have demonstrated proof at scale. Now the focus shifts from validation to volume.

Stablecoins, tokenized liquidity, and programmable settlement rails will not simply accompany the global payment system in 2026; they will begin to reshape its operating assumptions. The platforms that succeed will be the ones capable of translating technical maturity into predictable, repeatable financial flows.

AI Systems Begin Participating Directly in Payment Flows

In 2026, the most important shift around AI will not be better interfaces or faster models. It will be AI systems beginning to participate directly in economic flows. Protocols like x402, which define a native way for software agents to request, receive, and verify payment as part of an API interaction, point toward a future where AI is no longer just analyzing transactions but initiating and settling them.

This matters because it collapses a long-standing gap between computation and settlement. Instead of routing usage through subscriptions, credits, or human-in-the-loop billing, AI agents can transact in real time using programmable money.

Payments become atomic, machine-readable, and tightly coupled to execution. For infrastructure providers, this introduces a new class of counterparty: autonomous systems that require the same guarantees around settlement finality, reliability, and compliance as any other participant.

Onchain Money Markets Become The Treasury Management Standard

In 2026, the shift from demonstration to deployment accelerates. Enterprise teams have spent the last two years testing programmable payments inside controlled corridors. Those tests have created comfort, surfaced operational requirements, and clarified where programmable money must outperform legacy routes.

The next phase is scale: more live corridors, higher daily volume, and deeper integration into treasury operations. Businesses will increasingly treat stablecoin-based settlement as a normal option in their payment stack, not an experiment running alongside it.

Success will be measured not in announcements, but in uninterrupted throughput.

Winners To Be Defined Based On Interoperability

Tokenized T-Bills will move from “emerging asset” to “default short-term parking” for globally active firms. Treasury teams will lean on on-chain money markets for intra-day mobility, 24/7 liquidity, and cleaner reconciliation.

This shift will be driven by operational advantage and shifts in marginal efficiency across borders.

For the first time, corporate treasury functions have access to instruments that combine the safety profile of U.S. government paper with the settlement properties of programmable assets. The separation between “stablecoins for payments” and “tokenized T-Bills for yield” will feel like a unified liquidity fabric.

In 2026, platforms that stay rigidly attached to a single chain, a single architecture, or a single worldview will fall behind. Institutions will expect liquidity to move freely across L1s, L2s, bank rails, stablecoin networks, and tokenized money markets without sacrificing reliability.

The winners will be those that treat interoperability as a product requirement, not a marketing claim. Providers who can bridge payment rails, FX corridors, settlement layers, and compliance surfaces into a coherent experience will set the new standard for modern financial infrastructure.

That shift is already underway. The requirements are clear. Payments must run in production. Liquidity must move across borders, rails, and balance sheets without fragility. Interoperability is no longer a future ambition, but a present constraint.

This is the environment we built Noah built for. Operating real payment and settlement rails across regions, connecting stablecoins, tokenized liquidity, and traditional financial infrastructure into a single execution fabric.

Not as a theoretical solution, but as production-grade plumbing designed for carrying volume, withstanding scrutiny, and scaling alongside institutional demand.